Application of the geometric Brownian motion model in West Texas Intermediate crude oil price prediction

DOI:

https://doi.org/10.31943/gw.v14i3.546Keywords:

Crude Oil, Stochastic Process, Geometric Brownian MotionAbstract

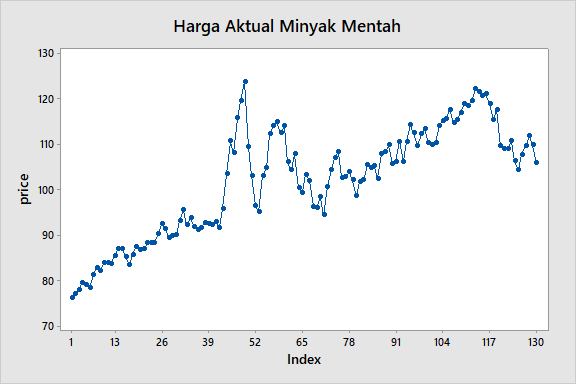

Crude oil is one of the primary commodities in the global economy. Crude oil prices are among the most complex and challenging to model because of the irregular, non-linear, non-stationary fluctuations in crude oil prices and their high volatility. It is essential to predict crude oil commodity prices to reduce the negative impact of fluctuations in crude oil commodity prices. Several mathematical models can be used to forecast crude oil commodity prices. One model that can be used is the Geometric Brownian Motion model, also known as the Wiener process. In this research, predictions for WTI (West Texas Intermediate) crude oil in 2022 were carried out using the Geometric Brownian Motion model. The results of this research are predictions of crude oil prices for July 2023 with iterations of 100, 200, and 1000, respectively, producing MAPE values of 6.092415%, 7.364198%, and 7.276606%.

Downloads

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2023 Vidya Dwi Pangestika, Farikhin Farikhin, Titi Udjiani

This work is licensed under a Creative Commons Attribution 4.0 International License.

The use of non-commercial articles will be governed by the Creative Commons Attribution license as currently approved at http://creativecommons.org/licenses/by/4.0/. This license allows users to (1) Share (copy and redistribute the material in any medium) or format; (2) Adapt (remix, transform, and build upon the material), for any purpose, even commercially.